How to Pay Off Credit Card Debt THIS YEAR

Are you searching for the quickest way to repay credit card debt while saving money and boosting your credit score? While the Avalanche and Snowball methods have helped many, the Debt Lasso Method is more effective. In this article, we’ll explore how this method helped us pay off over $51,000 in credit card debt in two and a half years and has helped our clients pay off over $1,000,000 in credit card debt.

Analyzing Credit Card Debt

The Impact of High-Interest Rates

The Debt Lasso Method originated from our realization that high-interest rates were a major obstacle to quickly becoming debt-free. With our interest payments reaching $10,000 annually, we devised a plan to reduce or eliminate this financial burden.

This could be you.

I believe now that my husband and I – will have an enjoyable retirement in Florida, and we won’t have to wait until I’m 75. – Fred N

We’re more prepared for emergencies than we have been long ago. I don’t like paying this bill [sump pump repair], but we now have the money to do it. We’re less stressed. – Karen D

My husband and I have traveled in the southern United States for four months. We’ve never had this much freedom. We couldn’t have done that if you didn’t help us pay off all our debt. – Claudia P

The Birth of the Debt Lasso Method

Through meticulous calculations and analysis, the Debt Lasso Method was born to cut down the time needed to pay off debt compared to traditional methods like the Avalanche and Snowball. The method aimed to pay off our $51,000 in credit card debt in three years, ultimately surpassing expectations by achieving this in just two and a half years.

Implementing the Debt Lasso Method

Overcoming High-Interest Rates

To execute the Debt Lasso Method, we engaged with their credit card companies to negotiate lower interest rates. Additionally, we utilized 0% interest rate credit card promotions, strategically transferring balances to minimize interest costs.

Refinancing Strategies

The method extends beyond credit cards, incorporating strategies for refinancing auto loans and mortgages. By refinancing to lower interest rates without extending the duration of the loans, individuals can accelerate debt repayment, save money, and improve their credit scores.

But the Debt Lasso Method isn’t just refinancing your debt; otherwise, everyone would be succeeding at paying off their debt. All five steps of the Debt Lasso Method are below.

Hear what we told Rachael Ray about the Debt Lasso Method:

How do I pay off my credit card with no money?

So, how do you pay off your credit card debt with no money? You probably noticed, as we did, that most of the money you send each month toward your credit card goes toward your credit card interest and not the amount of credit you’re using – your principal.

Credit card interest rates compound on themselves, and this “reverse savings and investing” makes it harder to become debt-free. That’s why you can send payment after payment, month after month, year after year, and you barely make a dent in your debt.

This is why most people think they need to make, find, or steal more money to pay off their credit card debt faster when, in reality, they need to put 100% of the money they’re sending to their credit cards and any extra money they have toward their principal (not their credit card interest).

This is how you can pay off your credit card debt with no more money than you’re already sending toward them now. This is why using the Debt Lasso Method to pay off your credit card debt over every other method you’ll find on the interwebs makes a lot of sense.

Refinancing your Debt and the Debt Lasso Method

The Debt Lasso Method wrangles your interest rates down as low as possible, ideally to 0%, to the fewest locations, ideally 1%.

Negotiating a lower interest rate on existing debt is possible. Still, you’re more likely to get Trump and Pelosi to skip onto the White House lawn holding hands than to get a bank to agree to a 0% interest rate – won’t happen.

That’s why the second and most productive step with the Debt Lasso for credit cards is using 0% interest rate credit card promotions.

So, first, we contacted all our credit card companies and asked them to lower our interest rates. Some agreed, even if it took some convincing.

Be friendly. Ask the rep for their name and use it up to three times. Ask them how they’re doing and share your story (don’t just ask for a freebie). For us, it helped that our payment histories and credit scores were good. The only thing holding us down was our debt/income ratios. The Debt Lasso works best with a better credit score.

Next, we used 0% interest rate credit cards with no annual fee offers. We calculate the balance transfer cost when we find these kinds of offers. This meant reading a lot of fine print and understanding what we read.

Most 0% interest rate credit card promotions last six to 18 months. The longer, the better. Longer terms reduce net expenses.

Then, we hustled to pay off as much of our credit card debt as quickly as possible. When one card was paid off, we put more money towards our remaining debt and repeated this until we were debt-free.

Refinancing your auto loan and the Debt Lasso Method

There are many reasons to refinance your car loan. The biggest is if today’s rates are lower than your current rate. Another is if your credit score has increased since you took out your last loan.

As with the credit card debt above, refinance your auto loan to a lower rate. In this case, don’t increase your time to pay off your debt. That’ll only increase your next costs. Keep the duration low.

Then, send 100% of any savings and extra money toward your auto loan principal. This, too, will help you pay off your car faster, save you money in the long term, and improve your credit score.

Refinancing your mortgage and the Debt Lasso Method

Refinancing your mortgage makes sense under certain conditions. People too often refinance mortgage debt and lower their month-to-month payments, then pay more because of extended terms or the number of years they have to pay off their mortgage. Likewise, refinance fees can make refinancing your debt for a mortgage cost-prohibitive.

Only refinance your debt for a mortgage if the refinance fees make sense, and you can keep your term between 10 and 15 years.

If you do a cash-out refi to consolidate debt, keep a loan to value on your property below 80%. Without at least 20% equity in your property, you’ll pay Private Mortgage Insurance. That’ll cost 0.05% to 1.00% of your loan.

A $300,000 mortgage costs $1,500 to $3,000 more monthly payments. Not worth it.

As with using the Debt Lasso Method for paying off credit card debt, using it for paying off mortgage debt will help you pay off your mortgage faster, save you money over the long term and improve your credit score. You’ll 10X this if you put 100% of any savings from your refi and any extra money toward your mortgage principal.

Is the Debt Lasso just debt consolidation or refinancing credit card debt?

5 Steps of the Debt Lasso Method

- Commit:

- Commit to stop using credit cards.

- Commit to paying more than the minimum monthly payment.

- Trim:

- Immediately pay off or trim cards that can be settled within one or two months.

- Lasso:

- Consolidate debt into as few locations as possible with the lowest interest rates.

- Automate:

- Automate credit card payments, focusing on paying more than the minimum on the card with the highest interest rate.

- Monitor:

- Ensure timely payments and adjust payments as credit cards are paid off.

The fine print (the tiny stuff) of the Debt Lasso Method

Read the fine print of any offer, understanding potential consequences for missed payments and post-promotion interest rates. Regularly opening and closing loans can affect credit scores, emphasizing the importance of maintaining open accounts with long credit histories.

Should I keep my credit cards while paying off my credit card debt?

Strategically managing your credit cards is crucial when aiming to pay off credit card debt. The decision to keep or close certain cards depends on various factors, and understanding these nuances can significantly impact your financial journey.

One key principle is to maintain your oldest non-retail credit card. This card holds the longest credit history, constituting 15% of your overall credit score. Preserving this lengthy credit history can positively influence your creditworthiness.

Conversely, retail credit cards often come with higher costs and limited benefits. In many cases, closing these retail accounts can be a sensible financial move.

Regarding your other credit cards, keeping them open or closing them depends on your circumstances. Some individuals choose to retain all their cards, while others opt to close certain accounts to eliminate the temptation of further spending.

Despite concerns about increased credit utilization due to closing cards, this impact can be mitigated by employing effective debt payoff strategies, such as the Debt Lasso Method. By rapidly paying off your credit card debt, any temporary adverse effects on credit utilization become negligible over a short period.

Keeping or closing credit cards intertwines your unique financial goals and habits. Understanding the impact on your credit score and incorporating smart debt payoff methods will help you achieve your objective of paying off credit card debt efficiently.

How do I choose which credit card to pay off first?

In 2023, according to the New York Federal Reserve, Americans bore the weight of a staggering $1.08 trillion in credit card fees, underscoring the pervasive challenge of credit card debt. This financial burden not only hinders people from realizing their aspirations but also contributes to heightened anxiety and exacerbates mental health concerns.

Now, you’ve taken a commendable step towards financial freedom by committing to pay off your credit cards. The next hurdle? Strategically navigating through multiple cards with varying balances and uniformly high-interest rates.

Choosing the sequence to eliminate your credit card balances can be daunting, especially when faced with prioritizing among different cards. Some individuals even contend with managing over 20 cards, adding an extra layer of complexity.

The real dilemma for most lies not in the desire to pay off credit cards but rather in selecting the most effective method and determining the optimal order for repayment. It’s about sticking to a strategy until every credit card balance reads $0.

Enter the Debt Lasso Method – a choice that reflects your financial acumen. Despite consolidating your credit card debt to minimize locations and secure the lowest interest rates, the challenge persists as multiple cards and varying interest rates remain in the equation.

So, how do you efficiently navigate this terrain? Understanding the intricacies of the Debt Lasso Method and implementing a customized plan for your specific credit card landscape will be key. By doing so, you’re not just paying off credit card debt; you’re reclaiming control over your financial well-being, one strategic step at a time.

What credit card do you pay off first?

Efficiently paying off credit card debt involves a strategic approach tailored to your financial situation. Here’s a comprehensive plan to guide you through the process and achieve debt freedom:

1. Immediate Wins with the Snowball Method:

Start by seizing quick victories. If you can comfortably pay off any credit card within 1-2 payments, employ the Snowball Method. This involves tackling smaller balances first, providing a psychological boost as you witness tangible progress.

2. Optimize with the Debt Lasso Method:

If you boast a high credit score, embrace the Debt Lasso Method. Maintain a consistent minimum total payment while strategically allocating additional funds towards targeted cards. This approach aids in efficient debt reduction without compromising your credit score.

For those with a lower credit score, fear not. The Debt Lasso Method remains a powerful tool to elevate your creditworthiness while paying off debts. Its structured approach offers a pathway to financial recovery.

3. Strategic Debt Elimination with the Avalanche Method:

For a comprehensive debt repayment strategy, consider the Avalanche Method. Initiate by making minimum payments on all credit cards. Direct any surplus funds and savings towards the card with the highest interest rate. Upon full repayment, cascade the minimum payment and extra funds to the next high-interest card.

Continue this strategic snowball effect until every card is debt-free, systematically targeting and eliminating higher interest obligations first.

Integrating these proven methods into your debt repayment strategy empowers you to make informed decisions based on your unique financial profile. Whether you opt for quick wins, credit score optimization, or strategic interest rate targeting, the path to debt-free becomes clearer, one methodical step at a time.

How do I budget while paying off credit card debt?

Achieving the goal of paying off credit card debt is intricately connected to effective budgeting. Contrary to popular belief, budgeting and debt repayment are not mutually exclusive; they go hand in hand. A robust budget serves as the compass guiding your financial journey, shedding light on your money’s origin and destination.

The key lies in clarity – understanding the inflow and outflow of your finances empowers you to make informed decisions. The more precise your understanding of your financial landscape, the better equipped you are to curtail unnecessary expenses and redirect funds toward eliminating credit card debt.

Now, faced with many budgeting options, how do you choose the right one?

The truth is, any budget is better than no budget. However, simplicity often triumphs. Our preference leans towards a straightforward spreadsheet that we crafted for our use. This uncomplicated tool proved more efficient than many available alternatives, even in the era of advanced apps. Surprisingly, we continue to rely on this trusty spreadsheet today, underscoring the timeless power of simplicity.

In essence, by harmonizing the act of budgeting with your mission to pay off credit card debt, you create a synergistic financial strategy. The clarity derived from a well-structured budget becomes your ally, allowing you to streamline expenses and channel more resources toward liberating yourself from credit card obligations.

Basic steps and strategies for starting to pay off debt

So far, we’ve talked about the quantitative steps for paying off credit card debt fast, but we haven’t discussed qualitative steps to take to pay off credit card debt super-fast. That’s important, too.

1. Adopt the mindset to pay off credit card debt (for good)

Indulging in designer clothes, extravagant vacations, and residences in prime neighborhoods, accompanied by prolonged happy hours—does this lifestyle sound familiar?

Some may label it as the “gay lifestyle.” A question once posed in an FB group echoes the sentiments: “Why does it seem so expensive to be gay?” If you’ve ever pondered this, you’re not alone.

The pursuit of keeping up with what’s perceived as the quintessential “gay lifestyle” left us, two discontented individuals, feeling like the epitome of the stereotype—looking fabulous but living fabulously broke. Picture it: sharing a two-bedroom apartment with three others in L.A. while cruising in Beemers and Audis.

One transformative evening, seated on the dining room floor of our basement apartment, we declared, “Enough!” The weight of our debt had plunged us into depression and frustration, masking the reality of the life we desired behind a façade.

Attempts to rectify our financial situation had failed before. We couldn’t continue living this way; a change was imperative.

Perhaps you find yourself yearning for something different.

Embarking on any transformation necessitates a shift in mindset. Wishing for change is one thing; believing it’s possible is another. But true transformation occurs when action follows. You’ll remain in the same financial predicament without altering your thought patterns or be back in debt.

So, consider this: altering your mindset is the first step toward a different reality. Embrace the distinction between merely wishing for change, believing change is attainable, and actively pursuing change. Your financial liberation begins with transforming your mindset, breaking free from the cycle of debt, and shaping the life you genuinely desire.

2. Have the vision to become debt-free

For many, a life without debt seems like an elusive dream—whether it’s the burden of student loans, credit cards, or medical bills. However, the perpetual presence of debt doesn’t have to be a fixed reality.

When we confronted our financial reality, facing a hefty $51,000 in credit card debt, we dared to visualize what life could be like without this burden. It was a transformative exercise. Consider this: the $10,000 annually spent on credit card interest payments became the catalyst for our dreams. We envisioned channeling that sum into maximizing our IRA accounts and embarking on adventures to Australia and New Zealand.

The joy of daydreaming was palpable. Conversations shifted from the constraints of credit card-induced hangovers to planning genuine vacations. We even explored the possibility of moving from our basement apartment to purchasing a condo.

So, what does your debt-free life look like? It’s more than a question; it’s an invitation to envision a life where financial constraints no longer dictate your choices. Imagine redirecting money once lost to interest into building a secure future or fulfilling lifelong dreams. The canvas of a debt-free life is yours to paint—what vibrant picture emerges when you envision financial liberation?

3. Get friendly with the Benjis

In the words of Macklemore, “Only got $20 in my pocket, I’m, I’m, I’m hunting. This is f*cking awesome.”

The true joy of managing your finances comes when you have a crystal-clear understanding of where the f*ck your money is coming from and where it’s going. It’s liberating to be in control. Establishing this awareness, knowing your current financial state, and envisioning where you want to be provide the indispensable roadmap to making your financial dreams a reality.

Our journey to debt freedom required that roadmap. Otherwise, the allure of Sunday Funday—popping bottles at happy hour and succumbing to the Amazon addiction—would continue to be the path of least resistance. After all, Mr. Visa and Madam Master Card never seem to utter the word “No.”

So, let me ask you: What brings you genuine joy that resonates days and weeks later, surpassing the fleeting happiness derived from impulsive spending?

An effective strategy we discovered: tracking it all becomes simpler when you opt for the tangible—cash. By embracing this method, you stay accountable and gain a clearer perspective on your financial landscape. It’s a powerful shift that lets you prioritize true joy over momentary pleasures, navigating the twists and turns of your financial journey with purpose.

4. Get ready. Get set. Go!

So, where the hell are you financially? By reading this far, you might have an inkling. Yet, as we all recognize, a notion is practically worthless unless backed by action.

How often have you conceived a brilliant business idea only to watch someone else seize the opportunity, turn it into reality, and reap the financial rewards? It’s a scenario many of us have experienced.

Confronting the reality of your financial situation—evaluating how much you currently possess about the life you’re leading and comparing it to what you need for the life you aspire to—is a powerful motivator for taking action.

Enough with the idle contemplation; it’s time to do something. The transformation you seek begins with awareness and purposeful steps forward. So, seize the moment, make those financial moves, and turn your aspirations into tangible outcomes.

5. Have the audacity to do it

Recall your last extraordinary first date – not the details, but the dynamics. Who took the plunge and asked the other out? It’s not about logistics; it’s about courage. And admit it, post that date, a certain happiness lingered (insert mischievous grin).

Now, think of your relationship with money. It’s not a marriage, but a simple step toward financial freedom is like asking your wallet to dance. Your future partner, your financial soulmate, will undoubtedly thank you. Because, let’s face it, nothing is sexier than a person with their life together, including their financial realm.

Speaking of romantic partnerships, did you know that couples – regardless of gender – who openly discuss money tend to have more fulfilling experiences in the bedroom? So, not only does financial responsibility make you attractive, but it can also contribute to better intimacy.

Meet people who’ve used the Debt Lass Method to pay off credit card debt

Because of the Debt Lasso Method, we’ve now paid off $60,000 in debt since February 2019. – Nathan E

I’ve paid off over $21,000 in credit card debt with the help of the Debt Lasso Method even while paying for my wedding and honeymoon. – Fred N

The Debt Free Guys’ Debt Lasso Method helped me realize my financial self-care is as important as other self-care for myself and our community. – Michael C

Because of the Debt Free Guys, my husband and I started our personal finance journey. We eliminated our credit card debt in less than a year with all the tips they provided. – Claudia P

It’s easy to keep swiping the card without considering the consequences. With the Debt Free Guys, we found the help we needed to get us back on track. – Brandon & Alex B

Shout out to the debt-free guys saving me $150/month in interest [with their debt lasso method]. I look forward to being out of consumer debt much faster . . . total savings will be about $2,250. – M Morris

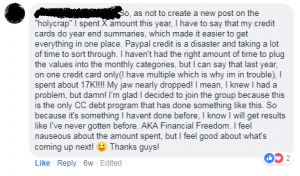

Since starting the Debt Lasso Method earlier this year, we’ve paid off $14,000 in credit card debt. – Karen & Dave D

I’m paying off $578 in credit card debt a month. – Jeanette

How Nathan and his husband paid off their credit card debt

Meet Nathan, a dedicated follower of the Debt Lasso Method who embarked on a transformative journey to repair his financial landscape. His initial breakthrough involved cultivating a keen awareness of his spending habits and the underlying motivations driving them.

When Nathan’s household income took a hit after his husband joined the military, an unanticipated challenge arose—maintaining their previous spending habits of a $125,000 annual income. Nathan’s long-standing practice of generously covering bills for friends, compounding the issue, contributed significantly to his accumulating debt. This financial strain intensified as Nathan, driven by his adventurous spirit, continued to travel extensively despite limited financial resources.

For Nathan, the perception of success was closely intertwined with his net worth, leading him to incur debt to sustain an outward appearance of affluence. His self-worth became tethered to the illusion of financial prosperity, driven by a belief that success was crucial for maintaining friendships.

The turning point came when Nathan’s husband was transferred to Japan, significantly reducing their expenses and motivating Nathan to address their financial challenges head-on.

Nathan attests to the pivotal role of the Debt Lasso Method, highlighting the invaluable weekly video calls as a cornerstone of the program. At the time of this recording, Nathan successfully eliminated over $21,000 in credit card debt. Impressively, his commitment endured, resulting in the full clearance of over $60,000 in debt. Nathan and his husband are focused on building a secure retirement fund, resuming travel, and sustaining their current lifestyle—all achieved through prudent cash management. Nathan’s story exemplifies the power of financial resilience and strategic planning in achieving long-term goals.

Fred and Rich threw a wedding, had a honeymoon, and still paid off $15,000

Enter Fred Norrell, once part of the 75% of Americans navigating their finances on a whim, as reported by CNBC. Fred’s financial journey took a transformative turn when he embraced the Debt Lasso Method, propelling him toward a debt-free existence and paving the way for the early retirement he envisions in the sun-soaked haven of Fort Lauderdale.

For Fred, the common belief that higher earnings would naturally lead to debt reduction proved to be a misguided assumption. Despite climbing the ranks with salary bumps and promotions, his debt and lifestyle expanded in tandem. With this perplexing reality, Fred turned to the Debt Lasso Method, initiating his financial overhaul with a profound revelation—the 12-month Spending Analysis.

This eye-opening exercise shattered his preconceptions.

Fred, known for his vibrant personality and generosity, often footed the bill for friends and his husband during nights out. The realization hit him (à la Blanche Devereaux) as he meticulously tallied up 12 months’ worth of bar tabs, restaurant bills, coffee shop receipts, vacation expenses, and the funds invested in his new vacation home. The sum left him wincing—a stark acknowledgment of unconscious spending habits fueled by the desire to keep pace with the proverbial “Joneses.”

Even as the awareness dawned, Fred and Rich had already committed funds to their wedding and honeymoon. Undeterred, they savored these moments while concurrently paying off a substantial $15,000 in credit card debt.

Joining the ranks of those who derive immense value from the Debt Lasso Method’s weekly video calls, Fred humorously dubs them his “money therapy.” His aspirations, shared with Rich, involve bidding farewell to high-stress jobs and embracing retirement in their Fort Lauderdale vacation home. Thanks to the Debt Lasso Method’s swift credit card debt elimination guidance, their dream inches closer with each passing day. Fred’s story exemplifies the potential for financial liberation and the pursuit of dreams through strategic debt management.

Why the Debt Lasso Method is the Best Method for everyone to Pay off credit card Debt

Are you wondering if the Debt Lasso Method is exclusive to gay couples? Think again. Meet Jeanette, a single woman thriving in the bustling heart of New York City, who credits the method with helping her conquer her credit card debt.

Just a year ago, Jeanette found herself in a financial abyss. Today, her perspective has undergone a complete 180, and she exudes confidence in her ability to conquer her financial challenges.

Jeanette’s financial odyssey began with a hefty $60,000 credit card debt. Attempting to alleviate the burden, she took out a $30,000 personal loan, only to find herself accumulating double that amount. A scarcity mindset compounded her financial woes as she grappled with guilt over spending beyond her means for her sister’s wedding. As the maid of honor, Jeanette felt compelled to host lavish parties, including the wedding shower, jeopardizing her financial stability for familial obligations.

Now aligned with the Debt Lasso Method, Jeanette envisions liberating herself from debt within four years, propelled by the method’s strategic approach and the invaluable weekly video calls. Once her debt is vanquished, Jeanette plans to redirect her focus towards hyper-focused investing for her long-term future, symbolizing a remarkable turnaround in her financial outlook. Her journey highlights the universality of the Debt Lasso Method, breaking barriers and offering individuals a pathway to financial empowerment, regardless of their relationship status.

Credit card debt knows no age and can still be paid off fast

Karen and Dave found themselves in a financial bind, grappling with unplanned expenses that pushed them to max out multiple credit cards. Faced with this challenge, they discovered a lifeline—the Debt Lasso Method—a decision that marked their investment in a debt-free future.

Karen, juggling full- and part-time work, was burdened by a staggering $700 monthly, translating to a whopping $8,400 annually, in credit card interest alone. On the other hand, Dave, in retirement, navigated the complexities of three different loans and debt across five credit cards. In the current interview, Karen’s monthly interest payments had already dropped to $500, and Dave successfully eliminated two loans and three credit card debts.

What makes Karen and Dave’s story stand out is its uniqueness, stemming from their financial struggles, age, and circumstances that led to their debt accumulation. Much of their financial burden originated from altruistic endeavors, notably supporting adult children with disabilities and other relatives. The repercussions of their generosity and other unconscious spending habits eventually caught up with them.

Yet, through their strides with the Debt Lasso Method, the dream of retirement is no longer a distant aspiration but a tangible reality. Their vision involves purchasing a trailer and embarking on a countrywide journey. With the progress they’ve achieved, the realization of this dream is imminent, signifying a triumphant turnaround in their financial journey.

Additional Debt Repayment Methods

While the Debt Lasso Method is the best way for most people to pay off credit card debt, it’s not the only way. Everyone’s situation is unique. There are tools for everyone.

Depending on your situation, some of the following options may be more helpful than the Debt Lasso Method to pay off your credit card debt.

1. Debt consolidation

The benefit of debt consolidation to pay off credit card debt is that you, hopefully, transfer all your debt to one lender – similar to the Debt Lasso Method. Also, like the Debt Lasso Method, you’ll go with the loan with the lowest rate.

However, unlike the Debt Lasso Method, you won’t find a 0%-interest rate loan no matter how good your credit score is. Finally, while origination fees may be comparable to credit card transfer fees, your consolidation company may tack on other, not-so-obvious, fees.

Regardless, this may still speed up your becoming debt-free.

2. Debt settlement

If you can’t afford to pay back what you owe on your credit cards but aren’t quite ready to apply for bankruptcy, debt settlement may be a solution – though not inconsequential.

With a debt settlement, you’ll pay back a percentage of what you owe – ideally, an amount you can afford – and your lenders discharge the rest.

Like bankruptcy, a settlement will appear on your credit report, hurting your credit score. Likewise, in certain situations, you may have to pay income taxes on the amount discharged, as your state and the federal government will see this as income.

3. Personal loans

The crux of the Debt Lasso Method rests on getting 0%-interest rate credit card offers. That’s not always accessible to people. The Debt Lasso Method can still be done with lower, not necessarily zero, personal interest loans.

If 0%-interest rate credit card offers aren’t available to you now.

4. Bankruptcy

Filing for bankruptcy is usually the last resort for most people. But, while it’s not the best experience in the world, it’s not the worst. There are different kinds of bankruptcies, including Chapters 7, 11, and 13.

5. Credit counseling

A credit counselor is a certified professional who helps you reduce your high-interest debt. If needed, they’ll put you on a debt management program. There’s for-profit counseling and non-profit counseling.

For-profit counseling charges you a fee, usually monthly. Non-profit counseling doesn’t charge a fee. In either case, you’ll continue to pay back your lenders, including any recurring interest agreed to in negotiations.

This service is great for anyone who needs some handholding, especially with non-revolving debt, such as mortgages, HELOCs, auto loans, and personal loans.

See what we told CNBC about the Debt Lasso Method:

Conclusion: Achieving Financial Freedom

In conclusion, the Debt Lasso Method is a powerful strategy to swiftly pay off credit card debt, save money, and improve credit scores. By addressing high interest rates and employing strategic refinancing, you can follow the five steps of the method to attain financial freedom.

While alternative methods exist, the Debt Lasso Method’s success in paying off millions in credit card debt showcases its effectiveness in achieving rapid debt elimination.

Other resources for paying off debt:

Thanks for the great advice you have given, I feel this is probably the best honest answer I have been looking for its also comforting to know that you guys are genuinely here to help . well forget the trim on budgets that benefit others , I am going to use a jigsaw to permenantly cut off expenses that create compound interest. Your advance has come absolutely on the brink of times.

Awesome article! Never heard about the Lasso Method before but it is brilliant. Never had debt myself so it was kind of interesting to read about it. I think Americans have a very special culture regarding credit cards. People in Europe doesn’t really live on credit cards. Could be interesting to find out how much debt average Americans have compared to Europeans.

Great article and btw I love the colours on your website. Especially the green one!